Your bank is funding war.

Canadian big banks invest heavily in weapons, military surveillance, and fossil fuel industries- fueling war, occupation, and climate disasters around the world.

All with YOUR money.

But you can do something about it.

Why Ditch Your Bank?

Investing in War

The Big Five Canadian banks—RBC, TD, BMO, CIBC, and Scotiabank—have invested over $14 billion in the top 40 global weapons manufacturers, including Elbit Systems, Lockheed Martin, and Raytheon, with billions more through loans and underwriting.

Fuelling Climate Disaster

The Big Five Canadian banks have pumped over $900 billion into fossil fuels from 2016 to 2023 alone. These banks are more committed to fossil fuel profits than human survival.

Financing Occupation

Canadian banks invest in over 112 companies listed by the UN as being complicit in Israel’s occupation.

Attacking Indigenous Communities

Banks continuously fund projects that violate Indigenous peoples’ rights at places like Standing Rock, Wet’suwet’en Yintah, and along the Transmountain Expansion.

Join a Credit Union

Credit unions are member-owned, cooperative financial institutions. This means they’re owned and controlled by the people who use them.

At credit unions, you’re a member/shareholder, not just a customer. This means you get a say in how the institution is run, which makes credit unions a more ethical alternative.

Many credit unions return profits to members as dividends, reduced fees, higher savings rates, or lower loan rates. Profits are also frequently donated or invested into local community initiatives.

Credit unions offer the same products and services as big banks! Your money is protected and government-insured, just like at a bank.

Find a Credit Union Near You

These are just a few of the larger credit unions in each province. All the CUs on this list offer in-person branches, ATM networks, mobile banking, e-transfers, and US dollar accounts.

Alberta

- Servus Credit Union

- Connect First Credit Union

- Vision Credit Union

British Columbia

- Vancity Credit Union

- Coast Capital Savings*

- Blueshore

Manitoba

- Assiniboine Credit Union*

- Me-Dian Credit Union

- Access Credit Union

Ontario

- Alterna Savings Credit Union

- DUCA Credit Union*

- Meridian Credit Union

- Kindred Credit Union*

Quebec

- Desjardins

- Caisse D’Economie Solidaire Desjardins

- Laurentian

Saskatchewan

- Conexus Credit Union

- Affinity Credit Union

- Innovation Credit Union

New Brunswick, Nova Scotia, Newfoundland, Prince Edward Island

- Brunswick Credit Union (NB)

- East Coast Credit Union (NS)*

- Newfoundland Credit Union

National

- Outlook Financial - The only Indigenous-led CU in Canada, and they provide an excellent interest rate!

- Alterna Bank - Owned by Alterna Savings. Online only

- Motusbank - Owned by Meridian CU. Online only

- Laurentian Bank - In-person branches in Quebec only

What happens next?

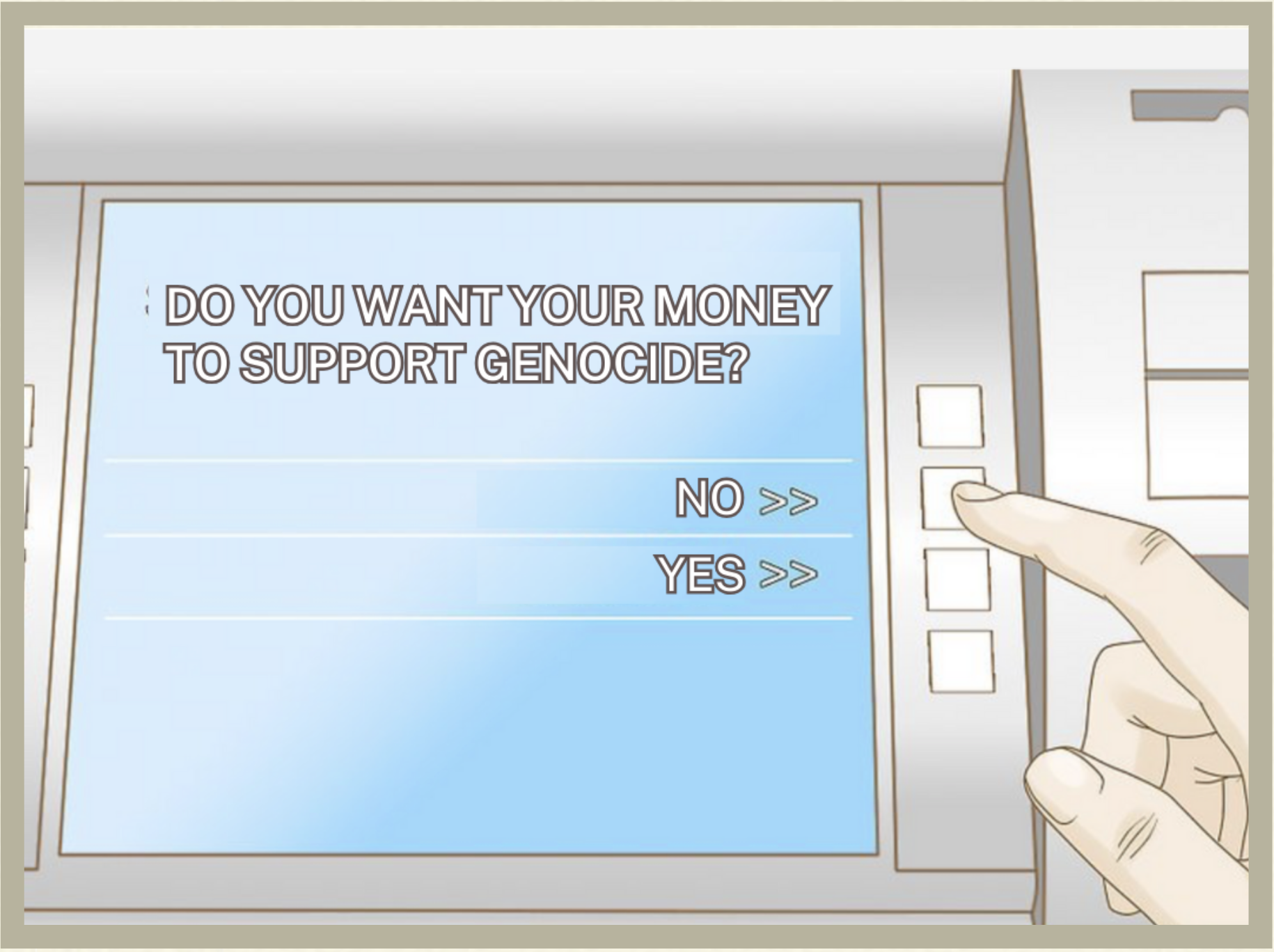

Your bank uses the money in your chequing and savings accounts to loan out to clients at a rate of $19x. This means that for every dollar you deposit, the bank can loan $19 to corporations that invest in war and environmental destruction (based on the Canada reserve ratio). The good news is that switching your chequing and savings accounts from a bank to a credit union is easier than you think!

Choose a Credit Union

Look into some different credit unions in your area to find one that best suits your needs. Look for competitive interest rates, low fees, and convenient branch locations.

Open an Account

Go to your new credit union’s website or visit an in-person branch to open an account. Fill out the necessary forms and provide any required documentation, such as personal ID.

Set up Mobile Banking and Transfer Funds

Go online or download a mobile app to set up your online banking account. You can transfer your funds from your bank account to your new credit union account online, or by visiting your branch.

Redirect Payments

Make a list of all your recurring payments and deposits, and redirect them from your bank account to your new credit union account.

Break Up With Your Bank

Go online or visit a branch to complete the process of closing your bank account. Speak with the bank manager, or send an email detailing your reasons for switching!

Join the Challenge

We know that dealing with your finances can be overwhelming. We’re here to help! Over the next 10 weeks, we will guide you through a step-by-step process to help you break up with your bank and start a new relationship with your credit union! From choosing a credit union, to switching your chequing and savings accounts, we’ve got you covered.

Thanks for signing up. We will be in touch soon!

FAQs

Is my money safe with a credit union?

Yes! Credit unions are regulated and insured in the same way as banks. The difference is that banks are federally insured, while the majority of credit unions are provincially insured. This actually works in your favour, because the federal government only insures your account to a limit of $100k, whereas provincial limits are $250k. This means that your credit union account is insured to a higher amount than your bank account! Look for your province’s deposit insurance or guarantee (DICO in Ontario) for more information.

Can I expect the same services at a credit union?

Credit unions offer nearly identical services as banks. You’ll often experience more personalized customer service, shorter wait times on the phone, and less employee turnover, meaning that the person you’re talking to is likely to have more knowledge and experience than a teller at the bank!

What about my mortgage/debt/lines of credit?

While it’s certainly possible to switch your mortgages, loans and investments to a credit union, you don’t have to take these steps in order to make an impact! The money in your chequing and savings accounts are what the bank uses to fund their unsavory investments. They cannot leverage your debt in the same way. We suggest switching your chequing and savings accounts to a credit union, and keeping your mortgages, loans, lines of credit, etc. where they are. We encourage you to shop around for a credit card that best suits your needs- that may mean continuing to use a bank-associated card, or signing up with an independent one. You will still be able to make all of your regular payments through your credit union account.

Will I still have access to ATMs if I switch to a credit union?

Yes! Most credit unions are part of a large national network that allows users to access ATMs surcharge-free nationwide. Visit dingfree.ca or theexchangenetwork.ca to find a connected ATM near you!

Where do I learn more?

Check out the amazing work these organizations are doing to help you take control of your money!

- Global Alliance for Banking on Values is a network of independent banks using finance to deliver sustainable economic, social and environmental development. Find out if your financial institution is a member here.

- BankTrack is an international organization that tracks financial institutions’ involvement with companies and projects that have a negative impact on people and the planet. Follow the link to find out if your bank is involved in any ‘dodgy deals’.

- Search Weapons Free Funds to find out if you’re investing in militarism.

- Decolonial Solidarity is a Canadian organization, comprised of Indigenous and allied supporters calling on RBC to end its funding of the Coastal GasLink Pipeline on Wet’suwet’en land.

- Change Course’s Banks off Campus campaign supports grassroots organizers on university and college campuses to get big banks off campus by focusing on student unions to divest from big banks.

- Just Peace Advocates is comprised of groups in Canada that support the global Boycott Israel movement targeting Israel’s system of settler-colonialism, occupation, and apartheid towards the Palestinian people.